“Don’t simply retire from something;

have something to retire to.”

Harry Emerson Fosdick

Personal Retirement Plan

Have your investments work for you. We are a team of qualified, experienced advisors that will maximise your retirement income by investing your pension assets and then giving your returns back to you. We will also help you to stay on track by providing with periodic portfolio reviews. Get back to doing the things you want to do.

If you currently have a pension with BIAS, click here to access your portal.

The Advantages of our Drawdown Product

Our drawdown product is a way of getting income by drawing money from your pension pot, while allowing your pension fund to continue growing. Instead of using all the money in your pension fund to buy an annuity, you leave your money invested and take a regular income directly from your funds.

Every year, you are entitled to a percentage of your total invested assets. This percentage is set by the pension legislation and may be received at a frequency that is comfortable for you, whether it is monthly, quarterly, semi-annually or annually.

The percentage rates set by the Bermuda Pension Commission are:

• Ages 55 to 64: 3% yearly maximum drawdown

• Ages 65 to 69: 7% yearly maximum drawdown

• Ages 70 to 80: 10% yearly maximum drawdown

• Ages 80+: 25% or $10,000 yearly maximum drawdown, whichever is higher.

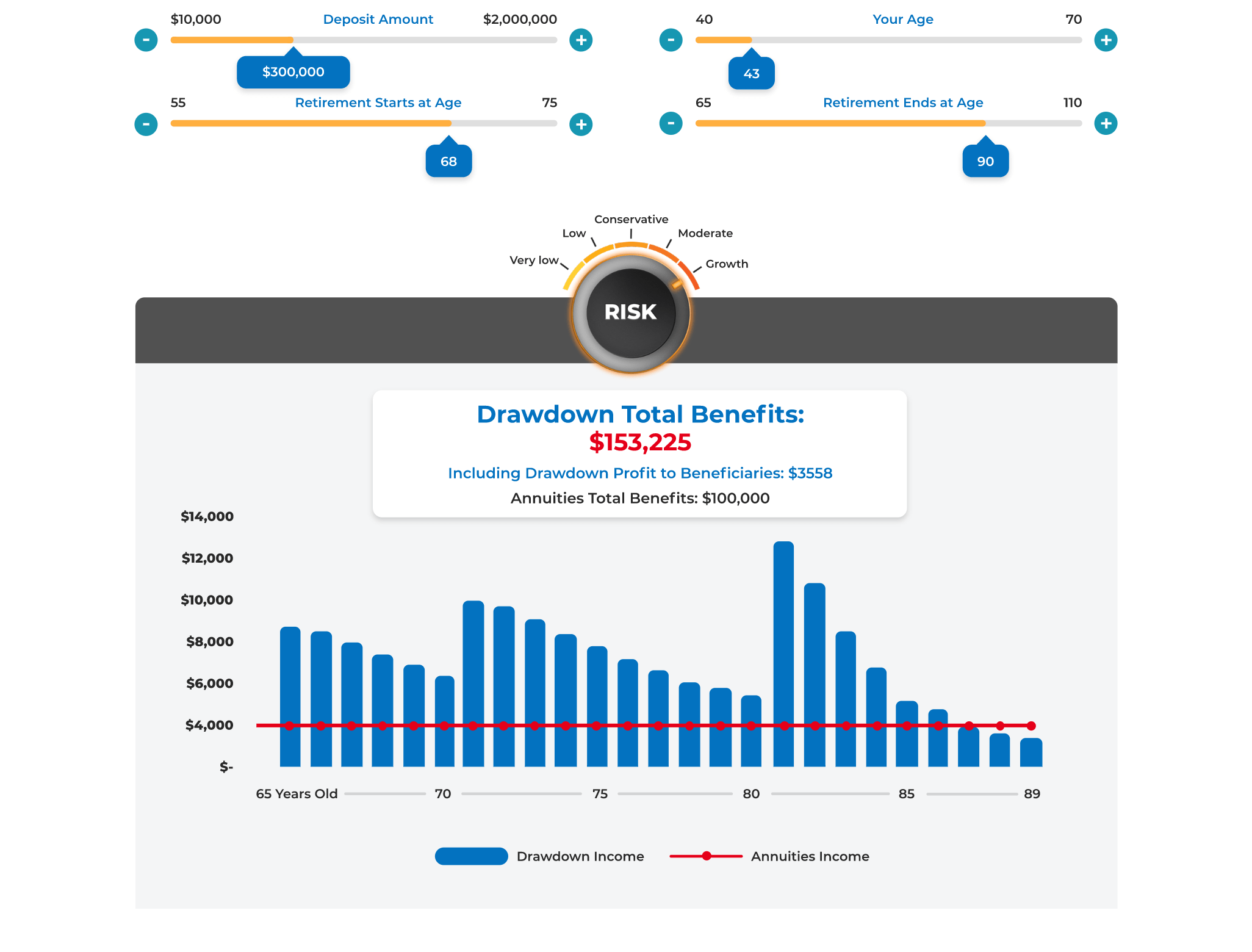

Dashboard

Use this dashboard to see what your drawdown benefits could look like compared with annuities.

Why Choose BIAS

We take the best care of our clients. In fact, we’ve had some of them for over 30 years.

Approved as a Pension Plan Administrator under the National Pension Scheme (Occupational Pensions) Act 1998. (Bermuda). BIAS Investors’ retirement plans are only operational in Bermuda.

Maximise Retirement Income

With BIAS Investors, you decide how much you will invest and where. By investing in the markets, you have opportunity to beat inflation with returns from your investments, maintaining your buying power as prices rise.

Hand-in-Hand Investment Management

We are with you every step of the way. A BIAS Investors advisor is available to discuss your risk tolerance, expected returns and formulate a strategy to help you achieve your retirement income goals. We are also available for periodic portfolio reviews to help you stay on track.

Maximise Growth

We use more than 30 years’ experience, intelligent research, and acute attention to detail when investing your retirement savings. You’ll get more out of your retirement benefit than what is available from insurance-sponsored plans. Between outperforming our competitors and our lower administration fees, we make sure your money goes back into your pocket.

Easy Portability

We make it easy to transfer your plan from any of the pension plan administrators.

Benefits go to Beneficiaries

With our drawdown plan, any residual benefits will be distributed to a maximum of four beneficiaries upon the death of the plan member. Unlike annuities, the profits go to you and your beneficiaries; not to the insurance companies.

Group Pension Solutions

We provide quality management, excellent customer service and performance not only for individuals, but also for groups.

Click here to learn more about our Pension Solutions for Groups →

Next Steps

- Fill out the Risk Profile

- We will schedule a meeting or a chat to provide guidance on which investment solution is right for you

- Scan in a copy of your utility bill (showing your physical address) and passport.

- Provide documentary evidence to support source of funds-pay slip, bank statement, job letter etc. (this is a regulatory requirement).

- Compliance will help you do the rest!